Initiating Insolvency Proceedings Against a Defaulting Borrower: A Complete Procedural Guide Under the Insolvency and Bankruptcy Code

The full Section 7 process, current timelines, and the 2026 amendment that just changed the rules for every lender in India

Introduction

For a lender sitting on a defaulted loan, the Insolvency and Bankruptcy Code, 2016 (“IBC”) is, in most cases, the fastest and most powerful recovery mechanism available in India today — faster than a civil suit, and generally more effective than SARFAESI or a DRT proceeding where the borrower has no easily enforceable security. But it is also a genuinely procedural regime: a defective Form 1, an incomplete record of default, or a wrongly chosen NCLT bench can cost months even in a case with an undisputed, indisputable default.

This guide walks through the complete procedure for initiating insolvency proceedings against a defaulting corporate borrower — the legal framework, the step-by-step filing process, the timelines that now apply, and the case law that has shaped (and, as of 2026, substantially rewritten) how Indian tribunals handle these applications. This is a particularly important moment to get this right: the IBC (Amendment) Act, 2026 has just fundamentally changed the admission standard for financial creditors, reversing years of uncertainty created by a single Supreme Court ruling.

The Legal Framework

Corporate insolvency in India is governed by the IBC, 2016, with the National Company Law Tribunal (NCLT) acting as the Adjudicating Authority. Three distinct routes exist to trigger the Corporate Insolvency Resolution Process (CIRP):

- Section 7 — filed by a financial creditor (a bank, NBFC, bondholder, or any person to whom a financial debt is owed under Section 5(7)).

- Section 9 — filed by an operational creditor (a supplier, service provider, employee, or worker owed an operational debt).

- Section 10 — filed by the corporate debtor itself, as a voluntary application.

The minimum default threshold is ₹1 crore, under Section 4 of the IBC, following the Central Government’s notification of 24 March 2020, which raised the threshold from its original ₹1 lakh. This threshold applies as of the date of filing the application, not the date the default occurred — a distinction the NCLAT has confirmed applies even where the underlying default predates the March 2020 notification.

This guide focuses primarily on Section 7, the route most relevant to a lender pursuing a defaulting borrower, with a comparative note on Section 9 procedure where the mechanics diverge meaningfully.

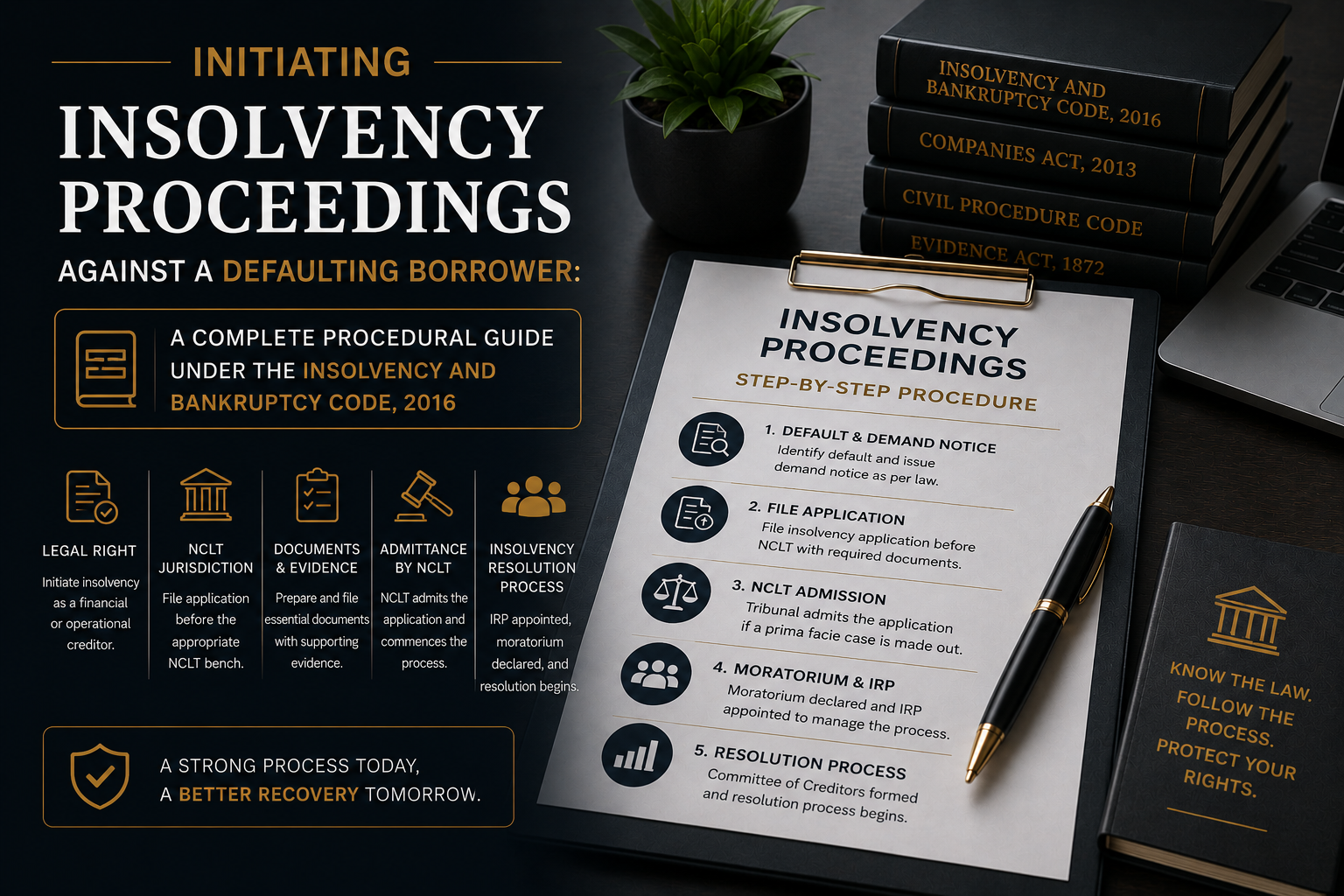

Step-by-Step: Initiating CIRP Under Section 7

Step 1: Confirm the Default and Assemble the Record

Unlike Section 9, a financial creditor is not required to serve any prior demand notice on the corporate debtor before filing under Section 7. The application proceeds directly to the NCLT. What it must establish, clearly and with documentary support, are two things: the existence of a financial debt, and default in its repayment.

The record of default is the evidentiary cornerstone of the entire application. Since the 2026 amendments, Information Utility (IU) records carry particular weight — where a financial creditor has reported loan data to a registered Information Utility (currently NeSL, India’s first operational IU), that record can substantially streamline the NCLT’s verification of default. Where IU records aren’t available or complete, the creditor must furnish other clear evidence — loan agreements, statements of account, certificates under the Bankers’ Books Evidence Act, and any acknowledgment of debt by the borrower.

Step 2: Prepare and File Form 1

The application must be filed in Form 1, prescribed under the Insolvency and Bankruptcy (Application to Adjudicating Authority) Rules, 2016 (“AA Rules”). Form 1 requires, among other things:

- Particulars of the applicant financial creditor and the corporate debtor.

- Particulars of the financial debt, with supporting documents.

- The date and evidence of default.

- The name and written consent of the proposed Interim Resolution Professional (IRP) — this must be accompanied by Form 2, the IRP’s written consent, confirming no disciplinary proceedings are pending against them.

- The relief sought — typically, admission of the application, declaration of a moratorium under Section 14, and appointment of the proposed IRP.

Jurisdiction: the application must be filed before the NCLT bench with territorial jurisdiction over the location of the corporate debtor’s registered office, under Section 60(1) of the IBC.

Limitation: an application under Section 7 must be filed within three years from the date of default, under Article 137 of the Limitation Act, 1963 (applied to IBC proceedings by the Supreme Court in B.K. Educational Services Pvt. Ltd. v. Parag Gupta and Associates (2019) 11 SCC 633). This period can, in appropriate cases, be extended through a condonation application under Section 5 of the Limitation Act, or reset where there has been a valid acknowledgment of debt — though the Supreme Court has recently clarified this is not automatic (discussed below).

Step 3: NCLT Review and the 14-Day Admission Timeline

Once filed, the Adjudicating Authority must, within 14 days, ascertain the existence of a default — from IU records or the other evidence furnished — and either admit or reject the application. If the application is incomplete, the NCLT must give the applicant 7 days to rectify the defects before it can reject the application on that ground; this 7-day rectification window is treated as mandatory, whereas the 14-day admission timeline itself has historically been treated by the NCLAT as directory rather than strictly mandatory, given how frequently tribunal backlogs push actual admission well beyond it in practice. The 2026 amendments have added fresh institutional pressure here — the NCLT is now required to record its reasons if it fails to pass orders within 14 days of receiving a complete application.

Step 4: Admission — What the 2026 Amendment Changed

This is the single most significant recent development for financial creditors. Historically, Section 7(5)(a) used the word “may” in relation to admission — a drafting choice contrasted against the mandatory “shall” used in the equivalent provision for operational creditors under Section 9(5). This apparently minor drafting inconsistency became the basis of the Supreme Court’s 2022 ruling in Vidarbha Industries Power Ltd. v. Axis Bank Ltd., which held that the NCLT retained genuine discretion to decline admission even where debt and default were clearly established — allowing tribunals to weigh a corporate debtor’s broader financial health, viability, and even a pending third-party receivable that might resolve the default independently.

The consequences were significant and, in practice, largely negative: NCLT benches applied this discretion inconsistently, some entertaining elaborate arguments about a debtor’s financial prospects while others applied it narrowly, producing forum shopping and prolonged, unpredictable admission hearings — the exact uncertainty the IBC was designed to eliminate in the first place.

The IBC (Amendment) Act, 2026 directly reversed this. The word “may” in Section 7(5) has been replaced with “shall,” removing the NCLT’s discretion to defer or reject a CIRP application once default has been verified through IU records or other evidence. Legal commentary is explicit that this amendment was introduced specifically to overturn Vidarbha Industries — restoring the earlier, simpler position that existence of financial debt and default in payment is sufficient, without inquiry into the debtor’s broader commercial circumstances. Several 2026 Supreme Court rulings have already reinforced this recalibrated position (discussed in the case law section below).

Step 5: The Admission Order and Its Immediate Consequences

Where the NCLT admits the application, it simultaneously:

- Declares a moratorium under Section 14 — this bars institution or continuation of any legal proceedings against the corporate debtor, prohibits transfer, encumbrance, or disposal of its assets, and suspends the recovery or enforcement of any security interest, effectively freezing the status quo for the duration of CIRP. The moratorium has narrow, defined exceptions — for instance, the IRP may continue supply of goods and services necessary to preserve the corporate debtor as a going concern.

- Appoints the Interim Resolution Professional (IRP) — under the 2026 amendment, the insolvency professional proposed by the applicant financial creditor in Form 1 must be appointed as IRP, provided no disciplinary proceedings are pending against them.

- Suspends the Board of Directors — management control shifts entirely to the IRP; the existing promoters and board no longer have authority over the company’s affairs.

Step 6: Public Announcement, Claims, and the Committee of Creditors

The IRP publicly announces the commencement of CIRP, inviting claims from all creditors within the timeline prescribed by IBBI regulations. Creditors submit their proof of claim — a financial creditor typically uses Form C under the IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016, a distinct filing from the original Form 1 application. Based on the claims received, the IRP constitutes the Committee of Creditors (CoC) — comprising financial creditors, who alone hold voting rights on the CoC (operational creditors, absent specific statutory categories, do not vote). The CoC then confirms the IRP in role, or replaces them with an alternative Resolution Professional (RP) of its choosing.

Step 7: Resolution Plan or Liquidation

The RP prepares an Information Memorandum describing the corporate debtor’s affairs and invites Expressions of Interest and resolution plans from prospective resolution applicants. The CoC evaluates competing plans and approves one by a 66% voting majority. The approved plan is then submitted to the NCLT for sanction under Section 31. If no plan is approved within the statutory timeline, or the NCLT rejects the plan submitted, the corporate debtor is ordered into liquidation under Section 33.

The Timeline: 330 Days, Hard Cap

CIRP must be completed within 180 days from the date of admission, extendable by a further 90 days with CoC approval — a combined outer limit of 330 days, inclusive of any litigation or appeal time. The Supreme Court’s ruling in Committee of Creditors of Essar Steel India Ltd. v. Satish Kumar Gupta (2019) confirmed this 330-day limit as the governing outer boundary, while also recognising that in genuinely exceptional cases — where the delay cannot be attributed to any litigant and extension serves the interest of all stakeholders — the NCLT or NCLAT retains limited flexibility to extend even beyond 330 days.

Section 9: The Operational Creditor Route, for Comparison

Where the claim arises from unpaid operational debt (goods, services, or dues owed to an employee), the procedure diverges in one crucial respect: before filing, the operational creditor must first serve a Section 8 demand notice. The corporate debtor then has 10 days to either pay the outstanding amount or raise a genuine, pre-existing dispute in writing. The Supreme Court’s ruling in Mobilox Innovations Pvt. Ltd. v. Kirusa Software Pvt. Ltd. (2018) 1 SCC 353 remains the leading authority here: if a genuine dispute existed before the demand notice was issued, the NCLT must reject the Section 9 application outright — a dispute conjured up only after the notice was served does not count, and the NCLT’s role at this stage is not to adjudicate the merits of the dispute, only to determine whether one genuinely, plausibly exists. This “pre-existing dispute” defence has no equivalent under Section 7 — a financial creditor’s application cannot be defeated merely because the corporate debtor disputes some other, unrelated aspect of the relationship.

Landmark and Current Case Law

The Foundational Cases

- Innoventive Industries Ltd. v. ICICI Bank (2018) 1 SCC 407 — the first Supreme Court ruling on the IBC, and still foundational. It confirmed that once a financial debt and default are shown, the Adjudicating Authority’s role at admission is narrow, and it settled that the IBC, as a central legislation, overrides conflicting state legislation (in that case, the Maharashtra Relief Undertakings Act) that might otherwise be invoked to delay proceedings.

- Swiss Ribbons Pvt. Ltd. v. Union of India (2019) 4 SCC 17 — upheld the constitutional validity of the IBC’s overall framework, including the differential treatment of financial and operational creditors.

- Mobilox Innovations v. Kirusa Software (2018) — the leading authority on the “pre-existing dispute” defence under Section 9, discussed above.

2025–2026: A Reset in Progress

- Vidarbha Industries Power Ltd. v. Axis Bank Ltd. (2022) — introduced discretionary admission for financial creditors, discussed above, now legislatively reversed by the IBC (Amendment) Act, 2026.

- Ecstasy Realty (24 February 2026) — the Supreme Court set aside concurrent NCLT and NCLAT findings that had refused admission based on an informally negotiated moratorium discussed only via email correspondence with one debenture holder. The Court held that a Debenture Trust Deed cannot be rewritten by informal exchanges, reaffirmed that the “pre-existing dispute” defence has no application under Section 7, and restored the company petition for admission — a clear signal of the post-Vidarbha judicial mood: once debt and default are established, admission follows, and tribunals should not manufacture equitable exceptions.

- State Bank of India v. Doha Bank Q.P.S.C. (28 April 2026) — arising from the Reliance Infratel insolvency, the Court held that liability arising from a corporate guarantee falls squarely within the definition of “financial debt” under Section 5(8), entitling the beneficiary lenders to be recognised as financial creditors — confirming that a guarantee, and not only a direct loan, can independently found a Section 7 application.

- Anjani Technoplast v. Shubh Gautam (23 April 2026) — an important limiting principle, and one every financial creditor should understand before filing. The Supreme Court held that insolvency proceedings cannot be used as a substitute for civil execution. Where a creditor had already obtained a money decree from a civil court and the decree had attained finality, initiating Section 7 proceedings instead of pursuing execution was held improper — the Court reiterated that the IBC exists for the reorganisation and revival of viable corporate debtors, not as an alternative debt-recovery mechanism for a claim already reduced to a decree, and imposed costs of ₹5 lakh on the creditor for misusing the process.

- Ankhim Holdings Pvt. Ltd. v. Zaveri Construction Pvt. Ltd. (2026) — confirmed that the mere pendency of a counterclaim for damages, or even criminal proceedings against officials of the financial creditor, does not bar initiation of CIRP — such matters have no bearing on the existence of the financial debt or the creditor’s right to invoke Section 7.

- A separate 2026 ruling clarified that a resolution professional’s mere admission of a creditor’s claim during CIRP does not, by itself, amount to an acknowledgment of debt that resets the limitation period for a fresh Section 7 application — a meaningful clarification for creditors relying on claim admission as a limitation workaround.

Structural Reforms Under the IBC (Amendment) Act, 2026

Beyond the Section 7(5) change, the 2026 amendment introduced several other structural changes relevant to anyone initiating or participating in insolvency proceedings:

- Creditor-Initiated Insolvency Resolution Process (CIIRP) — a new, out-of-court insolvency initiation mechanism, notably without an automatic moratorium. As of mid-2026, this and the accompanying cross-border insolvency framework had been introduced but not yet brought into force — worth monitoring, as it may eventually offer a faster, less tribunal-dependent alternative for straightforward cases.

- A new group insolvency framework has also been introduced, relevant for creditors dealing with corporate groups where multiple related entities are in financial distress simultaneously.

- CCI approval must now be obtained before a resolution plan is submitted to the Adjudicating Authority, rather than after — a sequencing change relevant to any resolution applicant, and a factor creditors should build into their timeline expectations.

- The Stakeholder Consultation Committee has been abolished.

- Resolution plans may now be approved by the NCLT in two phases — implementation and distribution — rather than as a single composite approval.

- CIRP restoration has been introduced as an option before initiation of liquidation — giving a further opportunity for revival before a company moves to the liquidation track.

- A resolution professional is now barred from subsequently acting as liquidator of the same corporate debtor — a conflict-of-interest safeguard.

- The Committee of Creditors must now record its reasons when approving a resolution plan, adding a documented accountability layer to what had previously been treated largely as a matter of unreviewable “commercial wisdom.”

Separately, the Supreme Court has itself taken suo motu cognizance of systemic delays in NCLT approval of resolution plans, flagging cases pending for nearly two years and directing both the NCLT Principal Bench and IBBI to address judicial and technical member shortages across benches — a signal that timeline discipline remains an active, unresolved concern even after the 2026 reforms.

Can You Pursue Other Remedies at the Same Time?

Yes. A bank or NBFC is not required to choose exclusively between remedies. SARFAESI enforcement, a DRT Original Application, and a Section 7 IBC petition can all be pursued simultaneously — the Supreme Court in Phoenix ARC Pvt. Ltd. v. Spade Financial Services Ltd. (2021) confirmed there is no bar against pursuing parallel recovery routes. What changes is the sequencing once CIRP is actually admitted: the Section 14 moratorium then stays further prosecution of any parallel DRT or SARFAESI action for the duration of CIRP, though it does not retroactively invalidate steps already taken. A creditor with multiple available remedies should typically pursue the combination most likely to produce leverage or recovery given the specific facts — not default reflexively to IBC alone, particularly where, as Anjani Technoplast illustrates, a matter that is really about enforcing an already-adjudicated decree is better pursued through execution than insolvency.

A Practical Checklist Before Filing

- Confirm the default exceeds ₹1 crore as of the date of filing, and gather Information Utility records or equivalent documentary proof.

- Check limitation — three years from the date of default under Article 137 of the Limitation Act, and don’t assume a partial payment or claim admission automatically resets the clock without checking current case law.

- Secure your proposed IRP’s written consent (Form 2) before filing, confirming no pending disciplinary proceedings.

- File in the correct NCLT bench — the corporate debtor’s registered office jurisdiction, not the creditor’s location.

- Assess whether the claim is genuinely a going-concern insolvency matter or, in substance, a decree-enforcement exercise — given Anjani Technoplast, using Section 7 as a substitute for execution risks not just dismissal but a costs order against the creditor.

- Consider parallel remedies (SARFAESI, DRT) where security exists, rather than relying on IBC as the sole route, particularly given ongoing NCLT timeline pressures even post-reform.

- Where the debt arises from a corporate guarantee rather than a direct loan, ensure the guarantee documentation and any hypothecation or related security is clearly assembled — SBI v. Doha Bank confirms this route is available, but it still needs to be evidenced properly.

Conclusion

The 2026 amendment to Section 7(5) marks the end of a genuinely turbulent five-year period in Indian insolvency law, during which a single word — “may” versus “shall” — determined whether a financial creditor with a clear, undisputed default could expect prompt admission or a prolonged, unpredictable hearing on the debtor’s broader commercial circumstances. With that discretion now legislatively removed, and a consistent run of 2026 Supreme Court rulings reinforcing that debt and default, once established, compel admission, the procedural path for a financial creditor is more predictable today than it has been in years — provided the application itself is built correctly from the outset, with a clean record of default, proper documentation, and a realistic assessment of whether IBC, rather than execution or another recovery route, is genuinely the right tool for the claim.

This article is intended for general informational purposes and does not constitute legal advice. Creditors considering insolvency proceedings against a defaulting borrower should have their specific facts, documentation, and recovery strategy assessed before filing.

If you are a lender or creditor considering insolvency proceedings against a defaulting borrower, or need your Section 7 or Section 9 application prepared and filed, feel free to reach out to VNC Corporate & Legal, Advocates & Solicitors.